Insights

February 2023 Market Commentary

By

Belvedere Group

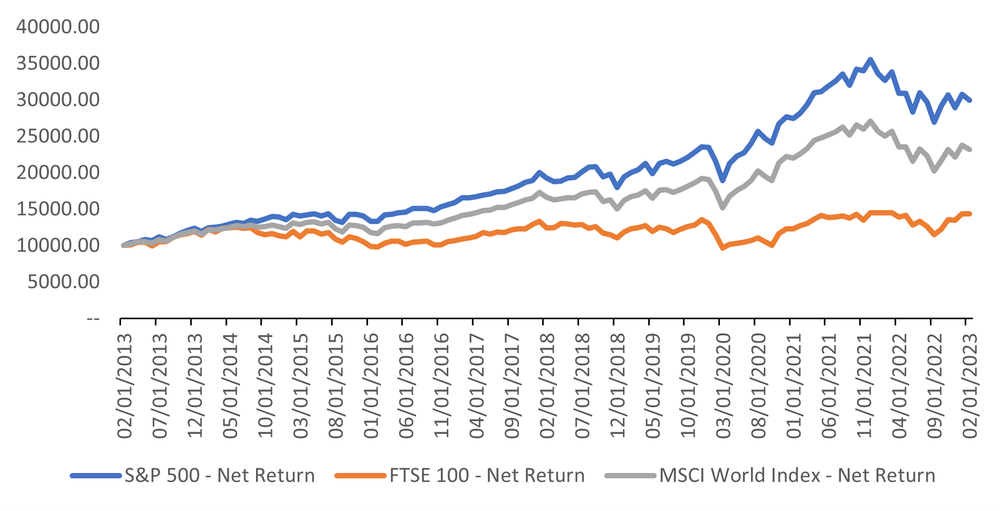

Following the close of the second trading month of 2023, an analysis of the developed markets reflects a positive year-to-date net return of 4.50%, outperforming the S&P 500 by 90bps, as the S&P returned…

Developed Markets Update

Executive Summary

• Nestlé sees record sales decline following price increases.

• United States review of economic indicators.

Markets Summary

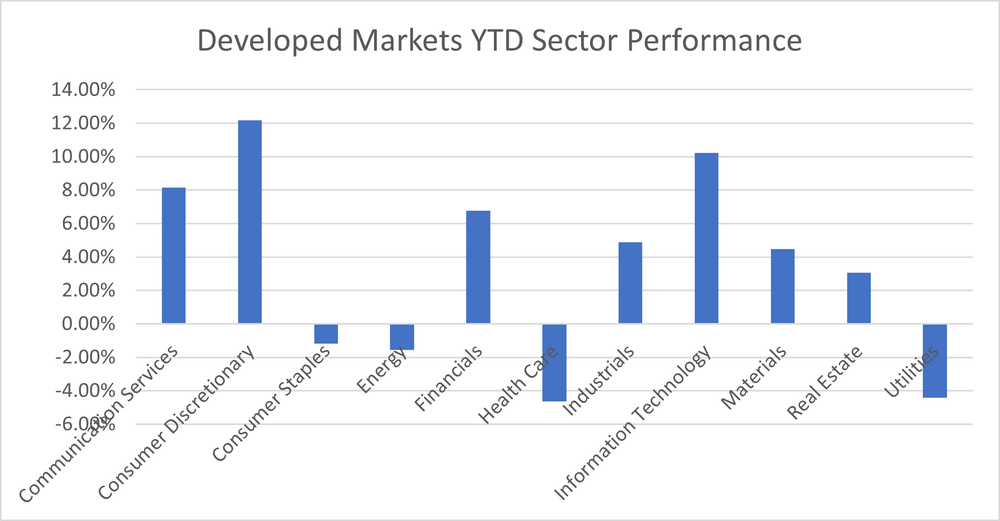

Following the close of the second trading month of 2023, an analysis of the developed markets reflects a positive year-to-date net return of 4.50%, outperforming the S&P 500 by 90bps, as the S&P returned 3.60% YTD. An analysis of the performance of the developed markets visualizes that the Consumer Discretionary and Information Technology sectors led the charge in driving YTD performance with a return of 12.16% and 10.22%. Both sectors had a contribution to return of 1.18% and 1.96% respectively. This supports our forecast in the January markets update, which states that consumer discretionary stocks will rebound as peak inflation and the pandemic headwind are behind us.

The Information Technology sector (IT) comprising 21.34% of developed markets stocks, thereby making it the largest, also experienced some positive tailwinds due to the transformational moments in AI from the launch of ChatGPT. The IT sector is important to pay attention to in 2023 as it generated over USD 2.5 trillion of revenue in 2022 to developed markets, with North America and Asia driving the majority of that revenue. In support of our thesis of staying selectively contrarian in 2023, we pride ourselves on the ability to capitalise on each of these trends to build long-term wealth for our clients.

Growth of $10K Relative Performance:

At home in the UK, 2023 brought with it continued momentum as Regulatory divergence is fast becoming a reality, as policymakers embark on a substantial review of financial services regulations following the UK’s exit from the EU. For legitimate reasons, the government wants a flexible framework that will make it easier for the Prudential Regulation Authority (PRA) and the Financial Conduct Authority (FCA) to regulate. As the newly appointed Chancellor Jeremy Hunt strives to reassure international markets, attract new business, and set global norms, it is clear that financial services and the City of London will play a significant role in the post-Brexit and post-pandemic reform agenda for the UK. The FCA warned firms about their readiness to comply with the obligations of the Consumer Duty as the PRA outlined its priorities for banks and insurers for the year.

Given that London is a significant global financial hub, the UK government wants to put in place several reforms that will make financial regulations in the UK more flexible, to stay agile in responding to new developments. Given this regulatory framework, we believe that this will increase the competitiveness of the UK market structure. The Bill must include a variety of measures about the future organization and structure of UK financial services regulation. Additionally, it contains the legal framework that will enable the government to progressively move the UK's regulatory framework away from a patchwork of inherited EU laws and add interim rules towards a more streamlined regulatory framework. The Bill is anticipated to become law at the earliest in spring 2023, ushering in a new era of autonomous financial policy-making in the UK.

Nestlé Sees Record Sales Decline Following Price Increases

The latest report from Nestlé, the world’s biggest food group, showed the company took a major hit with its volume of goods sold declining for the second consecutive quarter. In August 2022, the company increased prices by 6.5% in its attempt to cushion the effects of an increase in expenses, which according to its CEO Mark Schneider involved increased commodity, labour, and energy expenses. Nestlé increased prices for its products by an average of 8.2% across 2022 with sales growth mainly driven by price rises. Price increases by the Swiss group were highest in North and Latin America, at 11.6%. The increases affected the company’s North American sales volumes. Given this circumstance, we expect households in Europe and the US to continue switching to relatively cheaper options as the high level of prices reduces their purchasing power.

In Q4 2022, Nestlé made attempts to increase profit with the largest price hike on its coffee and noodles products. According to its CEO, the rising prices of its products are due to the global rising food prices caused by the war in Europe. Hence, this price rise by the company prevented Nescafé coffee and Maggi noodles from seeing an increase in sales. Hence, we forecast that as more consumers switch from Nestle, a trusted brand by most consumers to other products, this could cause a decline in the company’s sales and profits. As such, Nestlé might attempt to reduce prices. In addition, we expect the company to continue to use other measures such as cost and revenue management to cushion the effects of this decline in sales.

Nestlé Stock Price Chart Trend YTD:

We believe that Nestle’s long-term presence, which has created a strong brand awareness amongst its customers will continue to provide the economic moat that fends off its competitors. Nestlé benefits from economies of scale as it has averaged a gross profit margin of 48% over the last five years, which leads us to believe that it has the power to lower prices should it choose to. Although its net operating cycle has increased from 15 days in 2019 to 38 days in 2022, which was mainly driven by the fact that it held onto inventory 32% times longer in 2022 than it did in 2019, making us question its operating efficiency. We recognize the company’s efforts in launching affordable dairy milk in Pakistan, fortifying Maggi bullion in Central and West Africa, and leveraging local ingredients to facilitate supply and reduce costs. We will continue to monitor if this improves its fundamentals.

United States Review of Economic Indicators

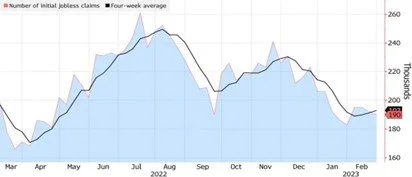

A reflection on the year 2023 has seen the US experience some positive headways with inflation slowing, growth increasing, and the slow pace of the Federal Reserve rate hike. The world's largest economy regained its ground at the end of 2022 after a difficult start to the year, with the US gross domestic product contracting in the first and second quarters of 2022, plunging Uncle Sam into the definition of a technical recession. However, GDP was quick to regain its footing, growing by 3.2% from July to September and 2.7% from October through December. These increases in economic output were largely driven by the steady increase in Americans’ spending. Similarly, the job market in the US has defied expectations after the pandemic outbreak in 2020, with record numbers in 2021 and 2022 in the country's books dating back to 1940. Hence, we expect the US to continue its positive recovery for growth for the rest of the year with inflation falling and interest rates declining.

US Initial Jobless Claims Sees Decline in Feb. 2023:

These impressive job numbers indicate the speed at which the labour demand is growing. We expect this to further entice the Federal Reserve to either maintain or hike interest rates in the forthcoming FOMC meeting. This is forecasted because an over-performing labour mark justifies the Federal Reserve’s stance on rate hikes as the apex banks seek to have a grip on price level to its preferred 2% range. The current benchmark rate ranges from 4.5% to 4.75%, the highest since 2007. Hence, we expect the early evidence of slowing inflation to entice the Fed to tamper with rate hikes in forthcoming FOMC meetings. This could see growth close to positive territory in the first quarter of this year.

Emerging Markets Update

Executive Summary

• Russia plans to cut its oil output by 500,000 barrels per day in response to the Western price caps.

• Chinese billionaire tech banker Bao Fan goes missing.

Market Summary

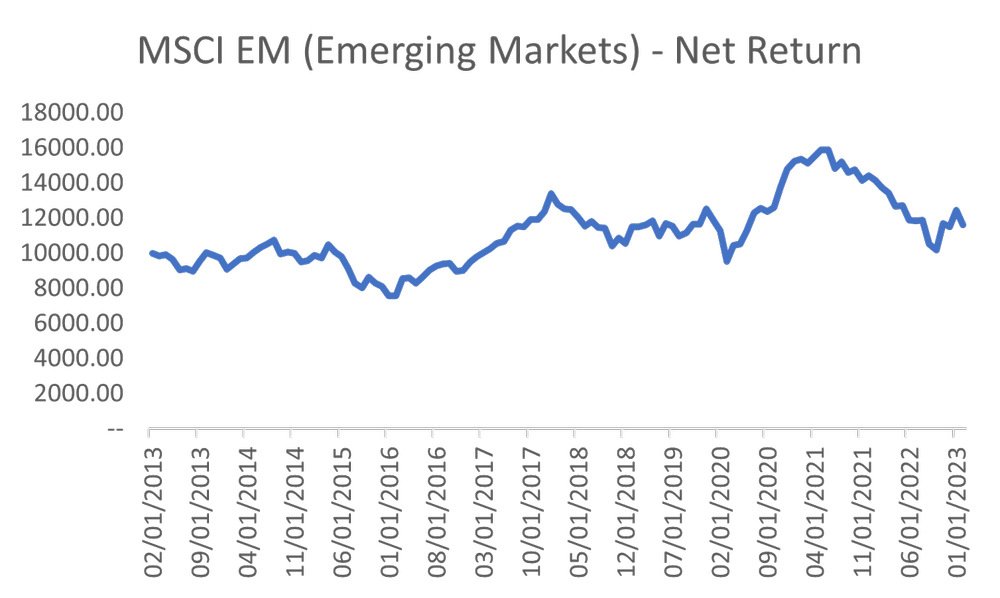

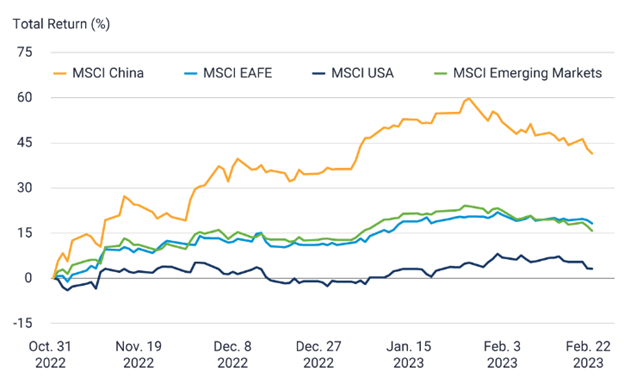

The MSCI emerging market (EM) broad index pulled back sharply by -6.48% making its worst February performance since 2001 after a bumper start of 7.91% in January. Geopolitical tensions contributed to the downbeat after the U.S. was set to expand the number of troops helping train Taiwanese forces, at a time of heightened tension with China and fears that U.S. interest rates would stay higher for longer demand for riskier assets.

As of February 28, the EM Index recorded a one-year net return of -7.33%, a three-year annualised figure of 9.90%, a five-year annualised return of 6.88%, and a 10-year annualised return of 8.77%.

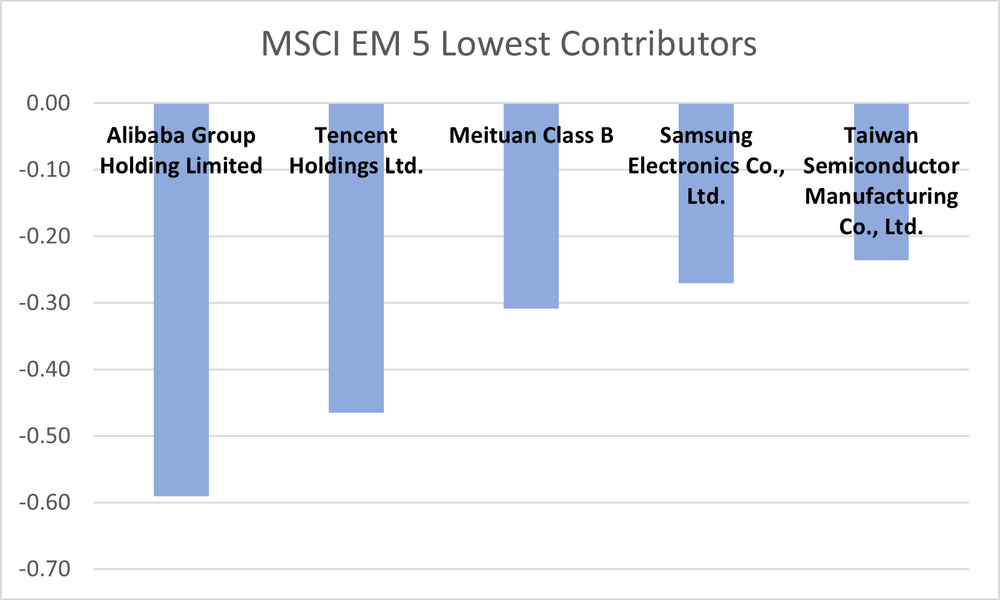

Large-caps EM stocks such as Taiwan Semiconductor, Alibaba, Samsung, and Tencent flipped upside down after recording a positive performance in January. The giant e-commerce (Alibaba) reported solid financial results for the fourth quarter of 2022. The company reported revenue that beat analyst estimates and due to the reopening in china, the company’s direct sales for its china commerce retail business rose nearly 10% and revenue increased by 2% year-over-year. However, the stock plunged as Hang Seng Tech stocks dropped amid worries that Beijing’s new regulations will hurt the outlook for corporate earnings of Chinese tech stocks.

Tencent Holdings Ltd shares sank 10.22% fueled by Tony Zhang Zhidong when he denied speculation about an unspecified, impending crackdown on china’s largest social media (Wechat). Despite the strong quarterly and annual earnings, Warren Buffett disclosed that he had sold most of his holdings in Taiwan Semiconductor but refused to disclose the reason. As a result, shares in Taiwan Semiconductor fell 3.54%. Following these recent updates, we expect stocks to close out the following month on a firmer footing as the large tech stocks seek to address the issues facing them. These and many other trends demonstrate the importance of having a long-term horizon in investing in EM.

EM MTD 5 Lowest Contributors as of February 28th, 2023:

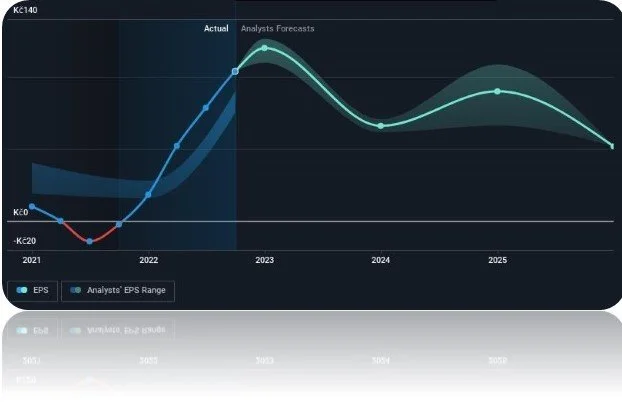

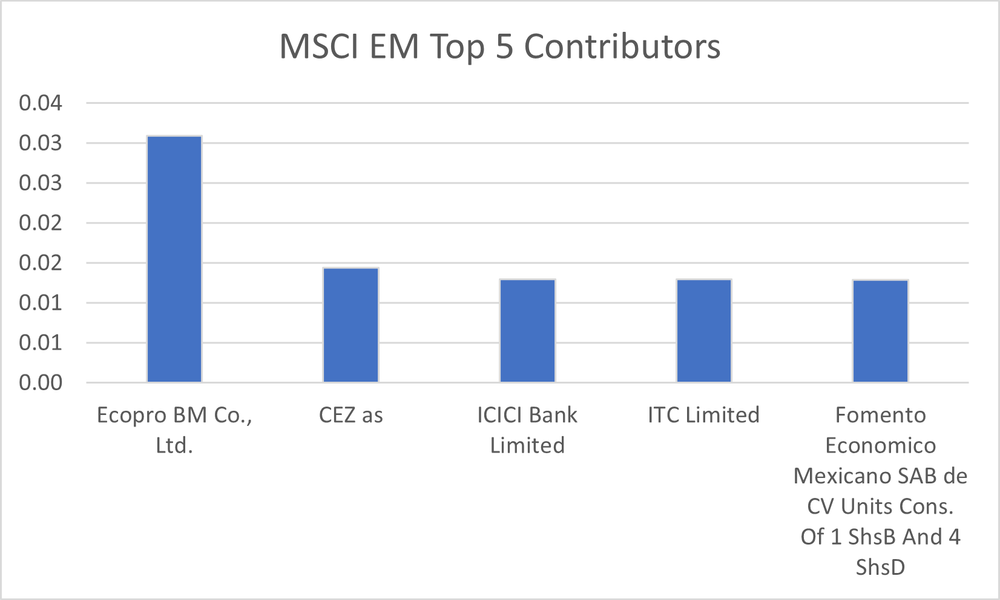

On the flip side, stocks performed better in other EM exchanges in the month of February. Looking at CEZ as’s share which has returned 103% in the last three years and a 22% gain in the last 3 months. During this period, the company has improved its bottom line, and the EPS of the stock moved from reflecting a loss to a positive gain over time. As shown below, the chart depicts the EPS growth trend and forecast. We observe that this has contributed to investors’ sentiment which led the stock to gain 15.40% in February. The shareholders of this company have received a return of 25% including a dividend over the last year.

In the Indian market, ICICI Bank Limited gained 1.85% in February. The Bank had signed an initial pact with BNP Paribas to cater to European corporate operations' banking requirements in India, establishing a partnership framework for providing financial services to corporate customers operating in India. The Indian conglomerate ITC Limited is the best-performing company in the NSE Nifty 50 Index this year, with a 15% gain. Shares of ITC Limited accelerated in February as investors began to place more emphasis on stability in a market that was roiled by concerns over corporate governance. According to a Bloomberg Economics review of governance, liquidity, and leverage at Indian conglomerates, the company comes out on top. Given this scenario, we believe that as investors continue to take interest in stable returns, this firm will continue to remain attractive.

EM MTD Top 5 Contributors as of February 28th, 2023:

The large tech stocks decline in February is simply the outcome of circumstances that are not anticipated to last longer for the long haul. Since investors' sentiment shifts in the same direction as forthcoming events, we anticipate a rebound in the future months. In a broader sense, we prospect that the inflation in Eastern Europe, Africa, and Latin America will undermine domestic demand as higher interest rates are combined with the region's rising cost of living. Yet, we forecast that the tech-heavy economies of China, Taiwan, and South Korea will be the main drivers of growth in the Middle Eastern and Asian economies.

Russia to cut oil production

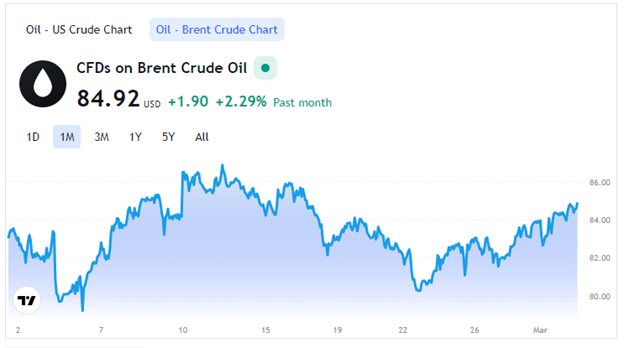

In 2022, western countries-imposed price caps on Russian oil and products. Russia responded by announcing its plans to voluntarily cut its oil production by 500,000 barrels per day in March. The cut which would be made from January levels amounts to 5% of Russia’s output and 0.5% of its global output. Russia has retaliated to a series of sanctions by diverting the majority of its oil exports from Europe to India, China, and Turkey. As a result, Indian, Turkish, and Chinese refiners flooded the market with fuels produced from Russian oil. Thus, Russia found it challenging to re-route exports of refined products away from Europe. Immediately after Russia disclosed its plan to cut oil production on Friday 10th February, oil prices skyrocketed in Europe, and the price of Brent crude was 2.5% higher on the day, and West Texas Intermediate rose similarly above $80 per barrel. Mr. Alexander Novak, the deputy prime minister and Russia’s point man on energy posited the production cut would contribute to the restoration of market relations and debunk the idea that Russia was facing challenges getting buyers for its product.

We do not anticipate the cut to throw the western market into a loop, given that it only accounts for 0.5% of the global oil. Western officials claimed that the cut was not big to pose a serious threat of disruption. The continent is anticipated to survive the winter without falling short on supplies.

China’s most influential financier (Mr. Bao) goes missing

Top internet businesses like Meituan and Didi are among Mr. Bao's clients. He is the CEO of China Renaissance and a well-known deal broker in China. A possible crackdown on Chinese leaders in technology and finance has been raised in light of this revelation. After the shareholders received the notice of the red flag, the shares of the investment company crashed. Afterward, it came to light that Mr. Bao was being held by anti-corruption authorities. In the past, billionaires have reportedly vanished for a while following purported encounters with the Communist Party, as stated by Forbes Magazine. Sometimes, they were thought to have been implicated in investigations into mischievous activities, tax fraud, and majorly corruption. Mr. Bao is regarded as a giant in China's tech sector because of the numerous transactions he completed that created the country's online consumer economy.